The official version of this document can be found via the PDF button.

The below content has been automatically generated from the original PDF and some formatting may have been lost, therefore it should not be relied upon to extract citations or propose amendments.

ST HELIER PARKING PRICING POLICY REVIEW EXECUTIVE SUMMARY

Parsons Brinckerhoff have undertaken a review of the likely impact of two parking policies for St Helier:

• Providing free parking at short stay car parks in St Helier on a Saturday; and

• Providing free parking at all car parks in St Helier on a Saturday.

This note provides the results from a series of small surveys undertaken on Saturday 19th October 2013 combined with other available datasets. The sample sizes were necessarily limited and due to timescales some data has been derived from aggregate figures or other assumptions. However this note intends to provide a first step estimation of:

• The likely benefit impact on retail sales in St Helier and

• The potential cost of the measures being proposed

We have used a high and low range for the estimated impacts. High forecasts take the more optimistic view of the success of the policies in creating additional trade to St Helier with the lowest cost impact.

Benefits to the Retail Trade in St Helier

The policy is designed to draw additional car-borne traffic into St Helier. The principal (but not exclusive) sources from which we expect the additional car-borne shopping, personal business and leisure activity to come from are:

Other out-of-town Observations on Saturday 19th October have provided an estimate of the shopping locations parking demand at a number of retail locations across the island. We have on island (such as suggested that the policy will cause a shift of between 3-5% of the 2,300 cars the Red Houses visiting other retail centres across the island into St Helier on a Saturday. precinct)

We have used a typical spend of £70 per car per trip, established from our town centre survey of car-borne shoppers, to provide a spend value each Saturday in St Helier.

Note, however, that this is re-distributed spend. It improves spend in St Helier to the same extent that it reduces spend in other locations.

Bus travellers who Surveys at the bus station on Saturday 19th October have revealed that 24% of switch to car in bus travellers had access to a car and driving licence for their trip (error range

response to the +/-11 percentage points)1. The remainder would be unaffected by any parking free parking, and pricing policy.

Bus Users Propensity to Switch Mode

Bus Users Propensity to Switch Mode

No car, no licence Licence, no car Stay with bus

Switch with Free Short Stay

Switch with Free Long Stay

Between 2-18% of total bus users would switch to coming to St Helier by car if the parking was free all day. This included a number of people with cars at home who were using the bus to come to work a full day in St Helier.

Those with cars making short stay trips by bus who would switch if the parking was free (for short stay parking) made up 0-11% of the total.

Liberty bus estimate 3,100 passengers made return trips into St Helier on Saturday.

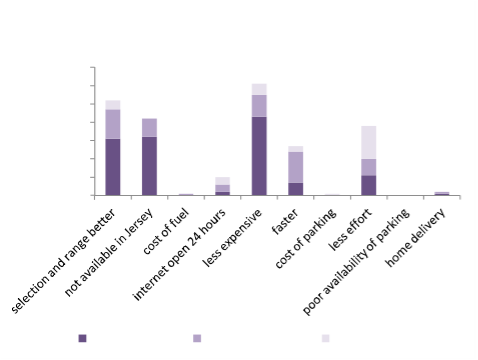

Spend that would The surveys undertaken asked why people had not used the shops for their otherwise have previous internet purchase. Reasons were:

been satisfied by

been satisfied by

the internet

Reasons for Using the Internet for the

Last On-line Purchase

70 60 50 40 30 20 10 0

Primary Reason Secondary Reason Third Reason

None of the respondents cited the cost or availability of parking as a primary factor.

The Office of National Statistics reports that around 9% of UK retail is undertaken using the internet. We have assumed a similar percentage for Jersey for a low estimate and 12% for a high estimate.

Car-borne respondents that had used the internet for a previous purpose were asked whether free parking in St Helier would have caused them to make their last internet purchase from a shop instead. Based on these responses we can estimate between 88-99% of the total population would not.

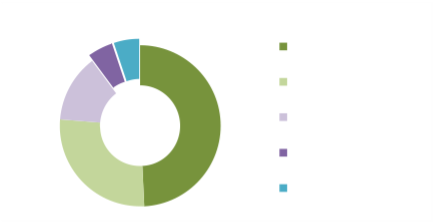

The following pie chart shows the low estimate of the retail spend that could transfer to St Helier from internet sales if free parking was provided. (This approach necessarily has to assume that the amount of internet spend by respondents is not correlated to their propensity to use shops if parking were to be free).

Total Retail Spend including internet

Total Retail Spend including internet

shop spend internet spend

internet spend switching to shop

Using data from the States of Jersey Statistics Department, we estimate that the spend on retail, personal business and retail leisure in St Helier on a typical Saturday is in the order of £1 million.

Summation of Benefits

A free parking policy would see the following increase in spend to town centre retailers.

High Low

Out of Town transfer £8,100 £4,800 Internet £15,500 £900

Bus Travellers transferring to car No retail change No retail change Total Spend £23,600 £5,700

Finally the total spend has been converted into a Gross Profit value to determine the value to the island economy from the purchase or spend. We have used a High Forecast value of 30% (for every £100 spent, £70 is average actual item costs which is spent outside the island providing the good). We have used a Low Forecast value of 15%.

High Low St Helier traders' benefit per Saturday £7,100 £900

Costs of the measures being proposed

There are three cost streams that we have calculated as consequences of the policy:

Lost trade to other shopping locations on the island

Bus Fare Loss

The Out of Town Shopping locations will lose a similar amount of retail and retail leisure spend to that gained in St Helier.

The number of current bus users that would transfer to using their car subject to free parking being provided will result in a loss to the bus operator fare box.

During our surveys on Saturday 19th October we obtained the fares being paid by those who said they would transfer to car under the policy. Assuming a full fare loss (and 75% fare loss for those riding on a zero fare concession), we have estimated the likely lost revenue to the bus operator under the policies.

Car Park Revenue With short stay free parking, sales lost have been applied to an estimate of

the amount of short stay parking on a Saturday. This is based on counts taken at car parks on a number of Saturdays during 2013.

With an all-day free parking policy, all parking sales for Saturday are lost.

As this estimate applies to existing use, it is the same for both the Low and High Forecast.

Summation of Costs

High Forecast

Out of Town transfer Bus Fare Loss2

Car Park Revenue Total

Low Forecast

Out of Town transfer Bus Fare Loss

Car Park Revenue Total

Short Stay Free £2,400

£0 £4,900 £7,300

Short Stay Free £700

£1,100 £4,900 £6,700

Long Stay Free £2,400

£200 £8,900 £11,500

Long Stay Free £700

£1,900 £8,900 £11,500

Net value of the policy

Benefits to Net Benefit St Helier Costs Net Annualised3

Benefit

Traders

HIGH Forecast Short Stay Free Policy Long Stay Free Policy

LOW Forecast Short Stay Free Policy Long Stay Free Policy

7,100 7,300 7,100 11,500

900 6,700 900 11,500

-300 -15,600 -4,500 -234,000

-5,900 -306,800 -10,600 -551,200

Notes:

- Error ranges have been provided based on a 95% confidence interval.

- While Out of Town transfers, and internet transfers are assumed to be higher in the High forecast, bus transfers, which create a dis-benefit for the policy, are taken to be lower.

- Car park utilisation data supports the use of an annualisation factor of 52.

25 October 2013

Supplementary Information

Other Free Parking Trials undertaken in St Helier Free Parking at Pier Road Trial

Free parking was provided at Pier Road for 5 Saturdays from 11th August 2012. Utilisation of Pier Road increased by approximately 100 vehicles. Observation by TTS parking staff based on time of entry and turnover indicated that this additional parking was composed primarily of long stay all day parkers who had transferred from other all day car parks such as Green Street.

Free After Three at Sand Street

The graphic shows the results from Springboard town centre footfall for week commencing 16th September 2013. This is the fifth week of a nine week trial during which Sand Street car park was free for parkers after 3pm. The utilisation shows that footfall on the Thursday is indifferent to Tuesday and anyway weaker after

3pm than a Monday or Friday.

The trial has been discontinued and TTS staff at Sand Street report that continuation of the trial in this format has not been supported by retailers.

TECHNICAL NOTE: PARKING PRICING POLICY REVIEW

Objective

In response to recent political statements in the local press suggesting that parking charges will be removed or reduced in some way we set out to understand:

• The potential cost of the measures being proposed; and

• The likely benefit impact on retail sales.

Approach

To allow us to estimate these components there are in essence two key themes we need to quantify:

• How much of the shopping spend in St Helier comes from existing car-borne trips; and

• How many more car-borne trips will arise from the new policy?.

We intend to answer the first by supplementing the shoppers' surveys already undertaken (in particular in 2012 and 2010) with a further High Street survey of shopping spend and modal choice to town.

We will answer the second question within the context of a Saturday by breaking it down into the three principal sources from which we expect the additional car-borne activity to come from. That is:

• How many of those trips will be abstracted from other shopping locations (come from Red Houses or other alternative shops)?;

• How many of those will be trips abstracted from the bus service?; and

• How many of those trips would have been satisfied by internet shopping?.

We can also consider the number of people shopping elsewhere or using the bus service during the week who would delay their trip onto a Saturday to take advantage of the uncharged parking. This has not been examined here.

Furthermore, to keep the study focused we will not collect quantitative evidence to determine

• How many trips that were walked or cycled will now be driven? (abstraction from slow modes); and

• Whether shoppers will come to St Helier more often (trip generation).

With the current workplan we will aim to demonstrate:

• What we can expect the additional car shopping volume to be and what that will mean in terms of spend in St Helier;

• Where this spend will come from? (other island shops, out of town shops or the internet); and

• How many people will switch from the bus (on a Saturday) and drive to do their shopping.

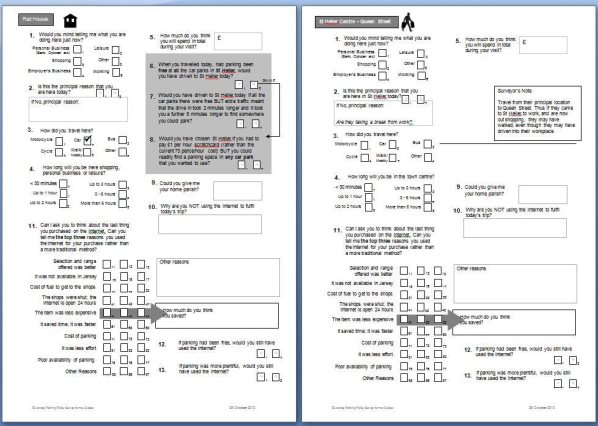

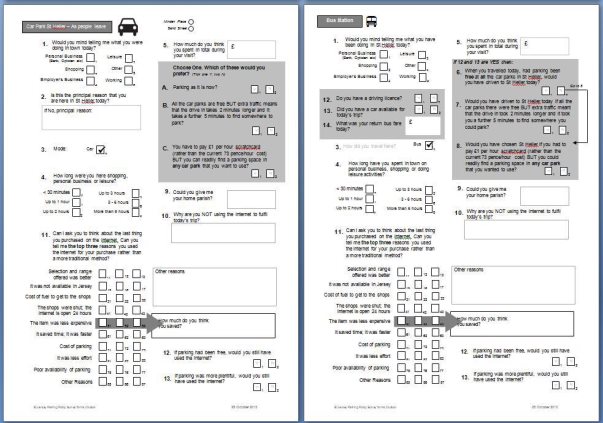

Data Collection

Parsons Brinckerhoff designed a series of survey forms and instructions for execution within Jersey on Saturday October 19th 2013 between 09:30 and 16:30. The survey was performed and data coded by the

States' own locally contracted staff.

Staff were deployed:

Timing Location Type Location

09:30-16:30 Out of Town Red Houses Precinct Car Park 10:00-16:15 Shopper Queen Street

13:30-16:15 Shopper Queen Street 10:15-13:00 Car User Sand Street Car Park 10:20-12:30 Car User Minden Place Car Park 13:15-16:30 Bus User Bus Station

The staff member provided for survey at Red Houses withdrew from the process. The total number of field sheets completed is presented below with a second line indicating those remaining after data cleaning. Respondents who were non-residents of Jersey were removed.

Red Car

Houses Centre Parks Bus Total Field Sheets 0 82 86 59 227

After Cleaning 0 80 82 59 221

Work Plan Flowchart

![]()

![]() The following flow chart sets out how we have estimated the modal share for those shopping in St Helier on a Saturday currently. Notes below refer to the numbers adjacent to boxes.

The following flow chart sets out how we have estimated the modal share for those shopping in St Helier on a Saturday currently. Notes below refer to the numbers adjacent to boxes.

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]() 01a

01a

![]()

![]()

![]()

![]()

![]() 01b

01b

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]() 06 02

06 02

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]() 05 03

05 03

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]() 04

04

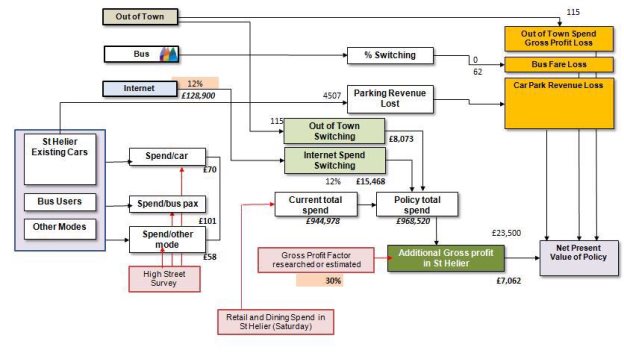

Out of Town Switching

Estimating the total volume of car-borne shoppers elsewhere on the Island in-scope to switch to St Helier is determined based on a) a Red Houses Saturday estimate and a b) other locations estimate ("01" in the figure above).

For Red Houses a 14:00 count of parked cars was made and factored by a space turnover factor to provide a total number of car trips to the location. This factor was derived from town centre interviews and is described elsewhere.

An estimate of other shopping trips that were non-local to other out of town locations and in-scope to switch will be made. This estimate is based on site visits and in consultation with officers.

Obs Red Houses Precinct 90 Red Houses Precinct Overflow 55 Red Houses Public CP 45 Red Houes Travel Agent 35 St Ouens Village 30 St John 35 St Peter Indstl Centre 50 St Peter Village 7 Gorey Harbour 30 Gorey Village 10 Ransons 20 Jackson s - St Peter Garden Centre - St Aubins Village - PowerHouse -

Total Out of Town (Saturday)

Assumed All Day 90 387

55 236 45 193 35 150 30 129 35 150 50 215 7 30 30 129 10 43 20 86 30 129 30 129 20 86 50 215 2308

The SP (Stated Preference) survey at Red Houses would have sought opinion of users' choice had non charged parking within St Helier been available for their shopping trip ("02"). The combination of these values provides an estimate of the number of car-borne shoppers using existing locations elsewhere that would switch to St Helier. Without an observed figure, we have used 3% and 5% (Low and High forecasts).

Internet

All surveys carried a question on respondents' last internet purchase ("03"). Value has not been sought, but reasons for using the internet in preference to shopping have. Users were asked secondary questions that would understand for their last explicit purchase whether they would have bought that item from St Helier had parking been non-charged.

Data from the ONS suggests that 9% is a reasonable proportion of retail spend on the internet (data up to 2012). We have used the value of 9% of sales being made on the internet for our Low forecast. For a High forecast we have used 12%.

Internet sales as a proportion of all retailing UK

12 10 8 6 4 2 0

|

|

|

|

|

|

We asked those interviewed for our surveys to consider their last purchase by internet. We asked them whether they would have made that purchase in town had there been non-charged parking.

We have taken our calculated total retail spend for the day and then applied a factor to this as the amount of spend that would transfer to the town centre under a free parking policy. This factor is based on the number of respondents who said that they would have used the town if parking was free.

We recognise that there is a potential bias that those that use the internet for shopping may not have presented themselves for a survey in the town centre. However we are working on the basis that for most people the internet is complementary to their town centre consumption rather than either/or. There is also an issue that while we are asking about the last item, there may be considerable variation around the amount that some people spend compared to others and this may correlate to their attitudes to coming into town. For our method we are giving each response equal weight.

Bus Users

A survey of bus users at the bus station has provided us with the proportion who have a driving licence and car available for their trip ("04"). Fourteen out of 59 interviewed had both licence and car. These are those that could transfer. Furthermore, of those 14, only 8 or 14% were in town for shopping, personal business or leisure. The others were in town to work and stay for a long period.

Thus a key finding is that even if parking is made free, most bus users are unaffected. They are captive to the bus service.

We have established through stated preference if those that could transfer to car would transfer to car under a new tariff regime.

Shopping Streets

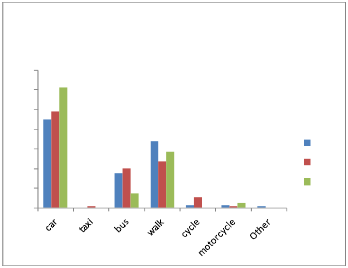

A random town centre survey of shoppers in Queen Street and King Street has provided us with details about their mode of access to the town. ("05").

Queen Street/King Street Shoppers' Mode

Queen Street/King Street Shoppers' Mode

70%

60%

50%

40%

2010 30%

2012 20%

2013 10%

0%

As shown we have cross referenced the car-borne share generated by this survey to other similar surveys undertaken in 2010 and 2012. Note that the 2012 survey shown in the graph is a combination of weekday and Saturday values. Our 2013 day has significant rainfall periods which could have suppressed walking and bus use although this could also be a response to the Saturday and a different type of person out shopping; where we have broken out the 2012 data below it indicates that there is more car-borne trade on the Saturday compared to the weekday.

For our work we have used the 2012 Saturday mode split.

2010 2012 2012 2013 (weekday) (Sat) (weekday) (Sat)

2010 2012 2012 2013 (weekday) (Sat) (weekday) (Sat)

car 45% 55% 46% 61% taxi 0% 0% 1% 0 bus 18% 19% 21% 8% walk 34% 19% 26% 29% cycle 1% 6% 5% 0% motorcycle 1% 0% 1% 3% Other 1% 0% 0% 0% Total 100% 100% 100% 100%

Car Park Capacity

We checked to ensure that the absolute additional numbers of parkers calculated can be accommodated by the parking provision within the town ("06"). In undertaking our calculations we have assumed each internet transfer generates a separate car trip. Notwithstanding, there is sufficient capacity on a Saturday for the additional traffic forecast.

The following flow chart shows the transition from additional parking numbers to retail spend and value to the town centre trade.

09

09

07 08

Notes are again provided:

Spend

The random survey of town centre shoppers sought to understand spend in the town on the visit made ("07"). As we will have the mode of travel, this provides a typical spend by visit and mode for the day being surveyed.

Mode

1 m/c 2 car

3 bus

4 cycle

5 walk

6 other Total

no % Total/mode Av/mode

2 3% £300 £150 49 61% £3,440 £70

6 8% £605 £101

0 0% 0

23 29% £1,140 £50

0 0% 0

80 100% £5,485 £69

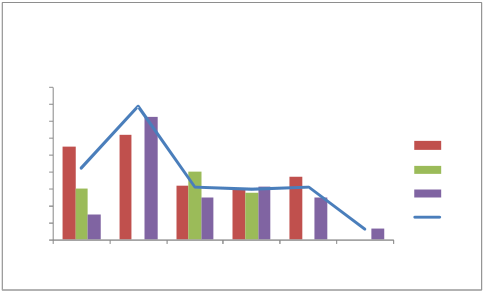

Spend per hour by duration and mode

Spend per hour by duration and mode

90.00

80.00

70.00

60.00 car 50.00

40.00 bus

30.00 walk 20.00

10.00 all 0.00

<30 < 1 hour < 2 hours < 3 hours < 6 hours < 8 hours minutes

This information is used as required to provide an estimate of spend, for example the out of town visitors that transfer to St Helier.

Data from the States of Jersey Statistics Team have been used to provide an estimate of retail and restauarant/bar spend in St Helier on a Saturday.

Jersey (retail) spending (source Stats Dept) excl internet Jersey (restaurants) spend (derived Household Spend) Total Spend in Jersey on in scope goods

Proportion of Jersey spend in St Helier (assumed) Proportion spent on a Saturday (based on car park use) Weeks in a year

Proportion that drive to retail (modal survey Saturday 2012)

Total Saturday Spend in St Helier on in-scope activities

£410,000,000 £112,476,000

£522,476,000 90%

0.19 52 55%

£944,978

Jersey retail spend derived by Statistics Team; restaurants/bar spend based on weekly household spend on these items x 52 x 42,000 households.

Gross Profit to St Helier traders

We have researched a factor to represent the overall gross profit value of Jersey town centre retail and leisure spend ("08"). Reports from the US suggest the range is from 25% to 50%. This factor, applied to the total spend will provide the Gross Profit remaining in Jersey. To represent that there is always a mix of products, we have used a factor of 30% for High and 15% for Low.

Out of Town Retail Loss

The number of shoppers transferring from out of town locations has been estimated as part of this work and we can provide a statement of the loss to these locations resulting from the policy ("09"). While St Helier retailers will gain, clearly other retailers on the island will lose out. This loss is not estimated to change whether St Helier operates a 3 hour or an all day free parking regime as all out of town shopping trips are expected to be less than 3 hours.

Bus Ridership Fare Box Loss

Some of those interviewed at the bus station that are currently using bus services indicated that they would switch to car if parking charges were changed. We have been provided with an estimate of the number of bus users coming into St Helier on Saturday 19th October by Liberty Bus. This estimate is

derived from the number of tickets sales from St Helier stops after 11:00. This is a proxy for those effectively buying the return portion of their trip. This number is 3,097.

We have applied the proportion indicating that they would change to car under a free parking policy to the total bus users estimated to be making a trip into St Helier on a Saturday. This provides us with a total number of switchers. More switch if the free parking is all day, as then it becomes attractive for those who said that they were working all day in town to also switch.

This then has been used to forecast the lost fare revenue to the bus operator. In doing this we have asked those using bus services how much their fare was and for pensioners, that pay nothing to ride the bus, we have used a claim of 75% of the adult fare for their trip (taken to be £1.70 each way).

Existing Parking Payment

For all existing car park users who will no longer be required to pay to park we have calculated the lost parking revenue arising from them ("10").

Net Present Value

The Net Present Value (NPV) is the summation of all discounted monetary costs and income streams (including additional spending).

Annual Review

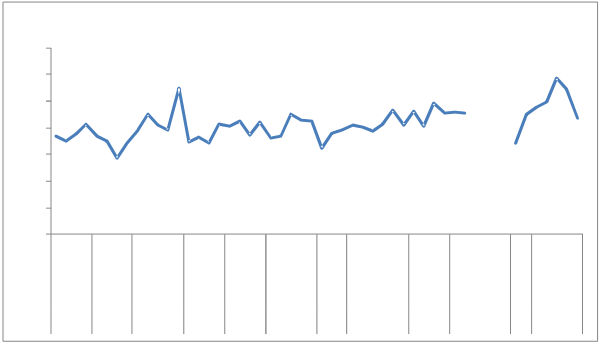

Data on parking usage over the year was be provided by TTS for transactions at Sand Street. This demonstrates that there is no significant summer peak. There is clearly an increase in parking activity in the approach to Christmas and a single spike for Easter. The intent to use results obtained from the October Week (baseline) and factor up and down to reflect a complete year is not warranted. We will annualise using 52.

Sand Street Transactions 2012-2013

Sand Street Transactions 2012-2013

3500 3000 2500 2000 1500 1000 500 0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Parking Preferences

Those interviewed in the car parks were asked if they would like to change the parking regime from its current arrangement. They were presented with three options (shown in text and pictorially):

Choose One. Which of these would you prefer? (Tick one Y, two N)

Choose One. Which of these would you prefer? (Tick one Y, two N)

- Parking as it is now?

- All the car parks are free BUT extra traffic means that the drive in takes 2 minutes longer and it takes a further 5 minutes to find somewhere to park?

Y N

1 2

- You have to pay £1 per hour scratchcard (rather than the current 73 pence/hour cost) BUT you can readily find a parking space in any car park that you want to use?

Y N

1 2

A B C

A B C

Driving

Time due to As now +2 Now other traffic minutes

Time

Searching An extra All Car Parks

As now

for a Car 5 minutes have spaces Park Space

Tariff per

73p No Charge £1 hour

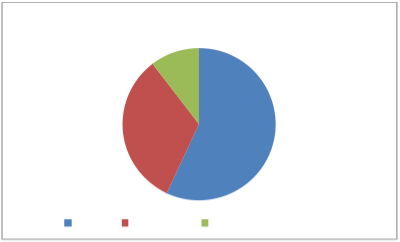

The majority (57%) of respondents were satisfied that the existing arrangement was most suitable. 28 (33%) did wish for free parking and would accept the deterioration in service. Notably 9 (10%) selected a higher charge if it meant that there was better parking space availability.

Parking Policy Stated Preference

Parking Policy Stated Preference

9

28

49

As now Free Parking Higher Charge; better access

Determining Short Stay Parking Volumes

Car Parks used for the town centre are:

Minden Place Charles St Provisional Ann Place Brewery Snow Hill Patriotic Street Green Street Sand Street Esplanade Pier Road

Charles Street Ann Place

Car Park occupancy data is available for counts at 08:00, 11:00 and 14:00 for Saturdays in February and June 2013. We have taken a mean of these two observations. To expand the data, all cars parked at 08:00 were considered to be long stay. In addition we have added 20% to this value for the long stay parkers assumed to remain within the car parks all day. We have taken a further 20% of the 08:00 parkers to be those who are short stay arrivals by 09:00. Car park occupancy for 10:00 is taken as an interpolation between the derived value for 09:00 and observed value at 11:00. Occupancy at 12:00 and 13:00 are interpolated between observed values at 11:00 and 14:00. Occupancies for each hour after 14:00 is taken to be 80% of the previous hour.

Parking TurnoverDu ¬ration

Average Stay was derived from respondents' statements at car parks on how long they were parking when interviewed. Assumptions regarding the actual stay length are shown in this table.

Taken from Car Parking Data 2013 | |||

Duration | No. | worth (minutes) | |

< 30 mins | 4 | 20 | 80 |

31-60 mins | 30 | 50 | 1500 |

1-2 hours | 35 | 105 | 3675 |

2-3 hours | 11 | 160 | 1760 |

3 – 6 hours | 0 | 240 | 0 |

More than 6 hours | 0 | 480 | 0 |

Totals | 80 |

| 7015 |

| average stay | 90 | |

The short stay volumes are used to determine a turnover rate for each car observed in the peak hour.

Total SHORT STAY car observations over the Saturday | 6761 |

|

Equivalent to | 405,630 | car.mins |

Average duration | 90 | minutes |

Number of SHORT STAY transactions | 4507 |

|

Total SHORT STAY car observations in the peak hour (that commencing 14:00) | 1049 |

|

Turnover | 4.3 |

|

HighLo ¬w Forecast Values used

The values used to determine the difference between the High and Low Forecasts are summarised here:

High Low out of town shopping 5% 3%

internet as % total spend 12% 9% % switching from internet 12% 1% bus short stay switching 0% 11% bus long stay switching 2% 18% Gross Profit Factor 30% 15%

Bus traders 35% 13%

Survey Results and Calculations held in Spreadsheet:Pricing Tool 05.xls

Survey Forms Used

Jersey parking Policy Forms 05.doc

Points of Scope

There is an argument that with lower parking charges people within Jersey may spend more on shopping and town centre leisure (coffee, meals out, discretional spend) that will come from other non-retail activities. So someone who may have spent Saturday afternoon watching the match on TV at home drinking beer from a can will now be attracted instead to watch the match in a town centre sports bar and drink beer from a glass. At a more extreme level someone who plays golf decides that the town centre now provides a more attractive location for a long walk and switches their spend from green fees to enjoying speciality teas. For simplicity and expediency, we have treated these types of transfers as out of scope. As a principal we have analysed on the basis that the retail spend by islanders is fixed. In truth the policy could divert spend from other activities and it is disposable income that is fixed [1] of which retail spend is a part. Thus retail spend could increase its share of total disposable income. The tariff change is not of sufficient magnitude

that this is likely to be a significant effect.

Allied to this it is worth noting that the approach taken to examine how internet purchases may be replaced by a town visit is effectively more trips by the same person. Our method has been to determine a typical spend value for an internet purchase. As a general rule and approach, however, we will make no attempt to forecast whether or by how much trip frequency to the town, or spend per visit, may change as a result of the policy and will assume no change.

We note that while the policy could also have impacts on the length of stay and amount that shoppers spend we have not attempted to quantify this through the survey.

An overriding consideration for St Helier is the seasonality of demand. During the summer months the number of visits to the town is swollen by tourists and holiday visitors. For our purposes all car-borne tourists are considered to be insensitive to the current parking cost tariff. Thus non-residents pay for parking without it having any bearing on their choice of destination or frequency of visit. The significance of this reasonable assumption is that the surveys can be baselined in October. Visitors in the summer months will continue to behave as currently and thus a reduction in parking charges will result in a net loss of parking revenue but no change in visitor behaviour.

When undertaking the random survey of spend within the town centre, the spend per car' was based on the total spend of the party interviewed. The assumption is that all party members are present and accounted for.

Those switching their shopping day

There are aspects of data collection that we consider to be out of scope for this particular assignment. The impacts must be assumed but these survey options could be undertaken and the assumed parameters in the tool could be replaced with empirical data gathered.

Survey

Bus users survey (weekday)

Town Centre Car users survey (weekday)

Out of Town Car users survey (weekday)

Mitigation

The number of bus users on a weekday transferring to car on a Saturday as a result of the policy is estimated

The number of car users on a weekday switching their day of travel to a Saturday as a result of the policy is estimated

The number of car users visiting a shop outside St Helier on a weekday switching their day of travel to a Saturday and location to St Helier as a result of the policy is estimated