The official version of this document can be found via the PDF button.

The below content has been automatically generated from the original PDF and some formatting may have been lost, therefore it should not be relied upon to extract citations or propose amendments.

Jersey Development Company's response to Dandara's high-level figures submitted to the Corporate Services Scrutiny Panel's review of the Jersey International Finance Centre.

Jersey Development Company (JDC) has reviewed Dandara's figures and attaches a financial summary and comparison that shows the States approved Jersey International Finance Centre (JIFC) generating a £52m return. JDC has responded on those figures that are not commercially sensitive and has kept the same rental figure and cost figures per Dandara's submission. Dandara has competing office schemes and it is therefore in its direct financial interest for the JIFC development to be stopped/delayed. Since 2000 Dandara has developed approximately 61% of all new build offices in St. Helier (since 2010 this has increased to about 69%).

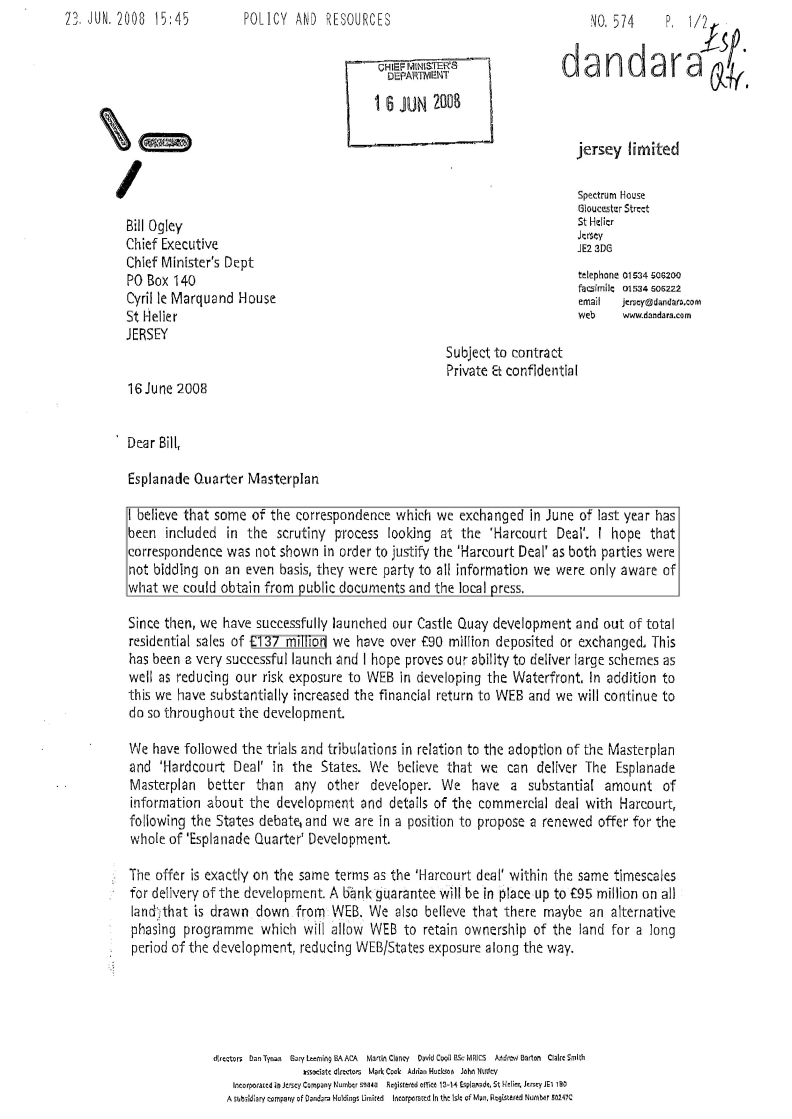

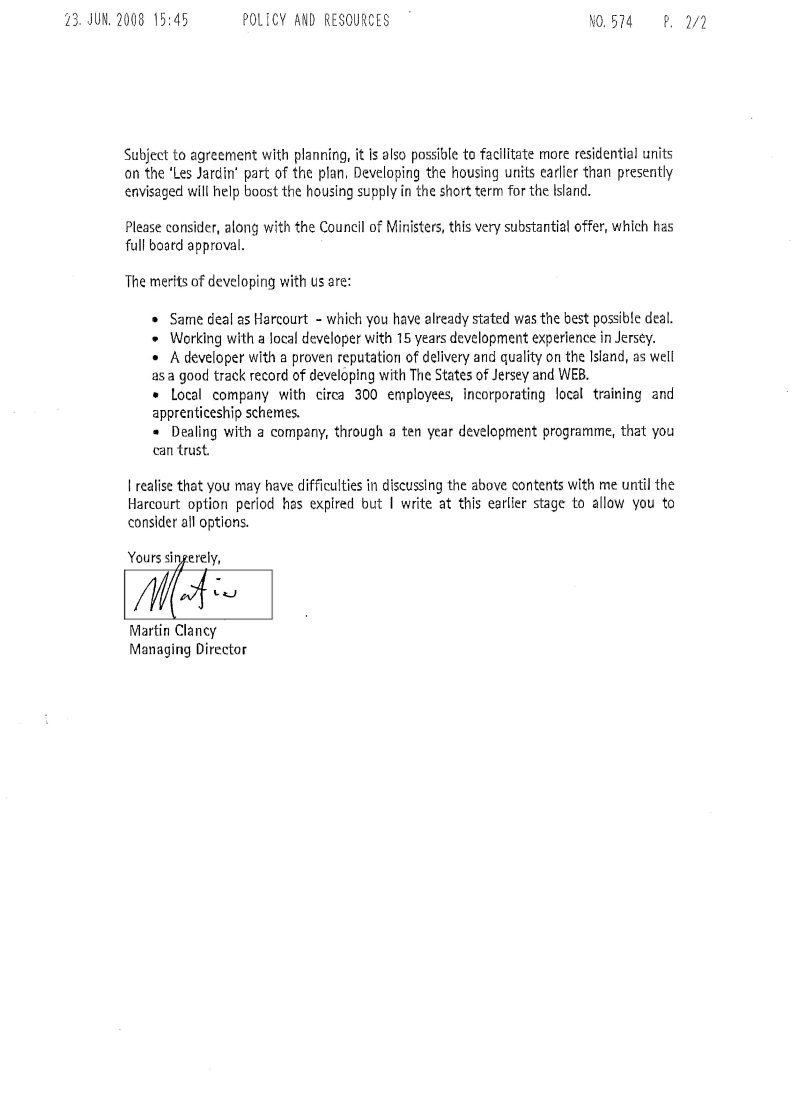

It is interesting to note that Dandara offered a bank guarantee of £95m for the Esplanade Quarter site in June 2008 and to carry out the Masterplan under the same terms as Harcourt Developments (letter attached). Since 2008, office rentals have increased from £27 per sq. ft. to £34 per sq. ft. (per Dandara's figures) and yet Dandara now claim the development will generate a loss?

The main items of variance are:-

- Yield:-

Dandara applied a yield of 7.15% and this is not considered to be reflective of the market. The value of prime central London offices is near its pre-recession peak and values in regional cities are now improving considerably. Investors are now returning to the Channel Islands where yields are looking attractive from a capital and rental growth perspective. Dandara refers to the recent sale of 44 Esplanade at 7.85%. The actual yield was 7.5% however this was a distressed sale and only had 7 years remaining to the first break clause (the lower the remaining term certain the higher the yield).

Non-distressed examples include Glategny Court in Guernsey which sold in August 2014 for £44m which represented a yield of 6.5% and in February 2015 Trafalgar Court in Guernsey sold for a consideration of £61.4m which reflected a net initial yield of 6.55%.

A yield of 6.5% (from Dandara's 7.15%) and using Dandara's rental figure of £34 per sq.

ft. improves the overall return by £30m.

- Rent Free Period:-

Dandara has deducted the rent free period from the end value at a cost of £20.5m. However, this scenario only prevails if the buildings are sold immediately on completion and JDC has always intended to hold the buildings until the expiry of the rent-free period (as Dandara has done with its office building at 37 Esplanade). By holding the buildings for the rent-free period improves the overall return by £13m.

- Land Value:-

Dandara has applied an inflated land value of £108.51 per sq.ft. of Net Internal Area

office. Based on Court documents, Dandara paid an average price of £62.19 per sq. ft for the sites at 66-72 Esplanade for its 160,000 sq. ft. office building that is currently under construction. Dandara has also ignored the fact that JDC already owns the Esplanade site and has therefore deducted its high assessment of net land value as a cost to the development – this is a manipulation to increase the alleged "loss" by £29 million!

JDC has always stated the £50+m net return from the JIFC development includes both land value and developers profit.

- Tunnel costs:-

JDC has always stated that the returns from the first phase of the Esplanade Quarter (the JIFC) would be needed to finance the lowering of Route de la Liberation. Dandara has added these costs above the line so as to increase the level of loss of the first phase. Dandara has also ignored the value of the development plots created by altering the road network (additional development plots will be created above the lowered road). These development plots have an estimated value of £25m.

JDC has been created by the States to deliver socio-economic returns for the Island. By undertaking the direct development of the JIFC the Island will generate in excess of £50m as opposed to an estimated £12m (post JIFC infrastructure costs) if the site were sold to a third party developer.

There is a finite demand for new office space and it is in the direct financial interests of competing developers to obstruct the delivery of the JIFC. In 2014 Dandara went as far as lodging a Third Party Planning Appeal in an attempt to thwart JDC's negotiations with a tenant (this Appeal was subsequently withdrawn).

Dandara's submission is the latest attempt to create concern and confusion amongst the public and States Members in the hope that the JIFC is delayed or derailed clearing the way for them to promote and complete their own schemes.

|

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

|

| |||||||

|

|

|

|

|

|

| ||

|

| |||||||

|

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

| ||||||||

|

|

|

|

|

|

| ||

|

|

|

|

| ||||

|

|

|

| |||||

|

| |||||||

|

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

| ||||||||

|

|

|

|

|

|

| ||

| ||||||||

|

| |||||||

|

|

|

|

|

|

| ||

|

| |||||||

|

| |||||||

![]()

![]()