The official version of this document can be found via the PDF button.

The below content has been automatically generated from the original PDF and some formatting may have been lost, therefore it should not be relied upon to extract citations or propose amendments.

Draft Damages (Jersey) Law

IFoA response to States of Jersey Corporate Services Scrutiny Panel

16 November 2018

About the Institute and Faculty of Actuaries

The Institute and Faculty of Actuaries (IFoA) is a royal chartered, not-for-profit, professional body. We represent and regulate over 32,000 actuaries worldwide, and oversee their education at all stages of qualification and development throughout their careers.

We strive to act in the public interest by speaking out on issues where actuaries have the expertise to provide analysis and insight on public policy issues. To fulfil the requirements of our Charter, the IFoA maintains a Public Affairs function, which represents the views of the profession to Government, policymakers, regulators and other stakeholders, in order to shape public policy.

Actuarial science is founded on mathematical and statistical techniques used in insurance, pension fund management and investment. Actuaries provide commercial, financial and prudential advice on the management of assets and liabilities, particularly over the long term, and this long term view is reflected in our approach to analysing policy developments. A rigorous examination system, programme of continuous professional development and a professional code of conduct supports high standards and reflects the significant role of the profession in society.

![]()

Corporate Services Scrutiny Panel 16 November 2018 States Greffe

Morier House

Halkett Place

St Helier

Jersey

JE1 1DD

Dear Sir/ Madam,

IFoA response to Draft Damages (Jersey) Law

- The Institute and Faculty of Actuaries (IFoA) welcomes the opportunity to respond to the States of Jersey Draft Damages (Jersey) Law. We are grateful for the opportunity to respond to a slightly later timetable, and this has given us more scope to consider the draft legislation in detail. However, in the relatively limited time available, there are aspects that we have not been able tofully consider or articulate in this response.

- Members of our Periodical Payment Orders (PPO) Working Party, General Insurance Standards and Consultations sub-Committee and General Insurance Board have all provided input to this response. Members of the Working Party, Committee and Board have worked closely on PPOs and personal injuryclaims over the last decade.

General Comments

- The IFoA is clear that the needs of injured parties should be at the centre of any compensation paid. We believe this view is consistent with the principles established inWells v Wells (1998), namely:

• 100% compensation but not more or less;

• that the claimant should be regarded as very risk averse; and

• the way in which the claimant uses the compensation is not relevant to its determination.

- The IFoA has a responsibility to promote actuarial science in the public interest. We have interpreted the public interest to be the requirement to provide appropriate compensation to the claimant in light of the above principles. If courts were to establish different principles for the settlement of claims, or if the Government of the States of Jersey were to re-define the policy purpose (eg the needs of the taxpayer, as opposed to claimants), we recognise the outcome for claimants and defendants would be different.

- As referred to in the draft legislation (Appendix 2), the IFoA responded to related UK Ministry of Justice and Scott ish Government consultations on personal injury/damages discount rates. We have drawn on points made in these responses below, where relevant; we have also submitted these responses with this one. As you will realise, these separate responses include points less relevant to the Jersey legislation; there are also some further specific features of the Jersey legislation not covered there, and we refer to these aspects briefly in this response.

- We would welcome the opportunity to discuss this response with the Scrutiny Panel in more detail. In particular, we would be very happy to provide oral evidence or any additional explanation of our comments if that were of value to the Panel.

Periodical Payment Orders

- The IFoA supports the use of PPOs, and the legislation prescribing the power to courts in Jersey to impose a PPO. Claimants in personal injury cases should be fully compensated, and as we have said in other responses, we believe that PPOs can often be the better solution for claimants.

- As noted in the draft Jersey legislation (background), PPOs can avoid some of the difficulties with lump sum awards in personal injuryclaims, including: the estimation of life expectancy; the concern that lump sum compensation could be exhausted before death; and managing uncertainty over future investment returns.

- In relation to managing longevity risk (estimating future life expectancy), it is important to recognise the specific characteristics of some injuries in personal injury claims. In some cases theymay have a direct impact on limiting lifespan. Other injuries may benefit from advances in medical treatment that can alter the life expectancy of a claimant many years after the claim settlement. Therefore the life expectancy of a particular claimant could be particularly influenced by their personal circumstances.

- It is also important to note that even if an individual's expected future lifespan is modified for circumstances at the time of claim, the individual will almost always live either longer or less than expected, with a significant chance of the lump sum compensation being exhausted before death.

- The IFoA would support an approach that considered a PPO as the preferred settlement option in personal injury claims. A PPO may not always be in the best interests of every claimant, but we would suggest that a lump sum alternative should be considered where the claimant or their advisors can demonstrate theyfully understand the risks of not accepting a PPO.

- It is also important to recognise that the nature of many personal injury settlements is such that PPOs and lump sum awards sit alongside each other; this point is acknowledged in the draft legislation. Both PPOs and lump sums can have a specific role within an overall compensation settlement. In an English/ Welsh context, PPOs are typically in respect of the cost of care only, although loss of earnings and case management costs may be included. That leaves many other heads of claim' that are settled bylump sum.

- This means there would not be cases settled only via a PPO. The PPO element is likely tobe the largest part of the total cost, when a PPO is part of an award. However, there are a number of situations where a PPO would likely not bemade available, and most of these revolve around the compensation level being limited.

- We note the draft legislation allows for PPO claimants to apply for a variation to their claim subject to their being a material change in their circumstances, but with no limit to the number of such variations. This contrasts with the situation in England and Wales, where there is an upper limit of one such variation. We can envisage debate over the materiality of any change in circumstances, and whether it then merited a variation inclaim. It may therefore be useful to provide further context on the requirements for such changes to be considered material, such as particular change in a specified medical condition.

- The intention of allowing multiple variations to ensure compensation remains fair following a change in a claimant's circumstances appears reasonable. However, it does give rise to a number of practical questions and potential unintended consequences:

• could PPO payments be reduced if appropriate, or would variation largely apply in one direction only (upwards)?; and if the latter would this be fair to all parties?;

• if PPO payments could be reduced, for example due to an unexpected improvement in the medical condition or injury (e.g. either through underlying improvement or due to a future medical advance), what would trigger a review?

• would there be an independent mechanism to monitor changes to a claimant's circumstances, and whether there had been a material change? Any such mechanism would also presumably come at a cost;

• if, in the absence of any independent monitoring, applications for a variation were triggered on behalf of the claimant, there may then be a bias to upwards variations in practice;

• if variation orders were expected to have an upwards bias, this could then have an adverse impact on insurers' capital requirements (see below).

- As acknowledged in the draft legislation, greater use of PPOs does pose challenges for non- life insurers in managing the associated risk exposure. The reserving and capital requirements of PPO are strong, and paying a lump sum in lieu of a PPO liability ismore certain, more straightforward and cost- effective for many insurers. There would also be further uncertainty over PPO valuation where multiple variation orders were possible. In addition, the longer term nature of a PPO liability is very different to the majority of (shorter term) liabilities of such insurers, which in itself has several implications.

- There are wider public interest concerns to consider, beyond the impact on a personal injury claimant. Where providing PPOs involves insurers taking more risk (compared with lump sum compensation), the investors of the insurers would require additional return to compensate for this additional risk. Any additional cost to insurers could result in higher insurance premiums, and this does have the potential to make insurance less affordable, and for some people, unaffordable.

- Some of the challenges and disadvantages of PPOs could be mitigated by performing a review of the structure of PPO settlement, for example by:

• alternative indexation of PPOs;

• pooling PPOs in an industry-wide scheme: and

• changing the way in which capital insurers must hold is calculated.

- Notwithstanding this however, it remains the case that any challenges insurers have in managing risks arising from PPOs are much less than the challenges individual personal injury claimants would face managing the same risks (future life expectancy, investment returns and associated costs). It is therefore important totake a broad perspective on the public interest, when considering the impact of legislation on personal injury claims.

The Discount Rate

- We note the proposal to set the discount rate by statute, replacing the current arrangement of being set by courts on a caseby case basis. As the draft legislation notes, this proposed approach has similarities with the corresponding legislation in England and Wales.

- We also note the recommendation to determine the discount rate from the expected returns from a low-risk diversified portfolio. Our view however is that the discount rate should be derived from a risk-free rate of return, reflecting the risk appetite of a risk-free investor. Lump sum settlements expose claimants to uncertainty over the adequacy of their compensation, and using a higher discount rate increases this risk. Note also that under Solvency II (the EU- wide insurance regulatory framework), insurers are required to use a risk free rate to value PPO liabilities.

- The representative portfolios used to derive the recommended discount rates include not insignificant exposure to equity and hedge fund investment. It is important to recognise that different individuals will have differing appetites to risk. Low, or very low risk for one individual maymean something different to someone else. Such differences in appetite will result in differing investment decisions. The variability arising from investment returns may provide additional assets for some individuals; but for other claimants, poor outcomes may lead to insufficient assets in the later years of life.

- The derivation of the recommended discount rate considers the relationship between RPI and wage inflation. Given that the long term payments being discounted are expected to be wage- related, we welcome this approach in establishing the rates. The assumed low risk portfolios are referred to as appropriate under proper advice'; however the rate derived does not deduct an explicit allowance for such expenses which is inconsistent. Furthermore, we believe allowance should also be made for investment expenses, including the cost of advice and ongoing investment fees/management charges.

- Uncertainty over wage inflation may however add a further layer of complexity. It is plausible that in a relatively small jurisdiction such as Jersey, care cost inflation could be quite volatile, depending on the availability of care expertise and on general demographics. This could make awarding of lump sums more uncertain for the claimant. For example, if the cost of care increased substantially to attract care expertise 10 years hence, would investment returns be able to cover them?A similar dynamic could make the valuation of PPOs more uncertain for insurers.

- Lump sum compensation may be exempt from tax but, whilst we are not familiar with the precise details of the taxation framework in Jersey, we presume that subsequent income from investing the lump sum would be subject to some form of taxation. For seriously-injured young people, the lump sum and hence annual income derived from this could be substantial. In such circumstances some tax may well be payable and this should also then be factored into the calculation of the discount rate.

- The draft legislation includes a provision that, following any subsequent review, the discount rate would be not be less than 0%. This restriction does not apply in England and Wales.We note the rationale for this limit: a negative rate would correspond to extreme (adverse) economic conditions, and under such circumstances, deviation from the full compensation principle could be considered more appropriate. However, personal injury claimants – given they would be seriously injured – may be particularly vulnerable during such economic conditions. It is therefore not clear to us that they would then bein relatively less need for full compensation.

- We note that the recommended discount rates are stepped' in nature i.e. 0.5% per annum if the expected loss is 20 years or less, and 1.8% per annum if the expected loss exceeds 20 years. Furthermore, the relevant single rate would apply for the duration of the claim, based on the expected duration at outset.

- The abrupt change in discount rate after a 20 year expected duration could give rise to practical difficulties where the expected lifespan of the claimant were around 20 years. Substantially different lump sums could be payable to claimants with 19 versus 21 year expected remaining lifespans.

- Where expected future lifespans were in the region of 20 years, the proposed stepped basis could then generate significant debate/ argument. One potential solution to this would be to apply a single discount rate to all claim payments within a specified duration, and then apply a separate discount rate to any subsequent payments. Using the duration/ discount rates in the draft legislation for illustration, this would mean applying a 0.5% per annum discount rate to all expected payments within 20 years from outset. However, a revision to the scope of any stepped discount rate should then reconsider the pre/ post step discount rates, and also timing of any such step.

Should you wish to discuss any of the points raised in further detail please contact me (steven.graham@actuaries.org.uk / 0207 632 2146) in the first instance.

Yours sincerely Steven Graham

![]()

Technical Policy Manager

On behalf of Institute and Faculty of Actuaries

The personal injury discount rate: how it should be set in future

The personal injury discount rate: how it should be set in future

IFoA response to the Ministry of Justice

11 May 2017

About the Institute and Faculty of Actuaries

The Institute and Faculty of Actuaries is the chartered professional body for actuaries in the United Kingdom. A rigorous examination system is supported by a programme of continuous professional development and a professional code of conduct supports high standards, reflecting the significant role of the Profession in society.

Actuaries' training is founded on mathematical and statistical techniques used in insurance, pension fund management and investment and then builds the management skills associated with the application of these techniques. The training includes the derivation and application of mortality tables' used to assess probabilities of death or survival. It also includes the financial mathematics of interest and risk associated with different investment vehicles – from simple deposits through to complex stock market derivatives.

Actuaries provide commercial, financial and prudential advice on the management of a business' assets and liabilities, especially where long term management and planning are critical to the success of any business venture. A majority of actuaries work for insurance companies or pension funds – either as their direct employees or in firms which undertake work on a consultancy basis – but they also advise individuals and offer comment on social and public interest issues. Members of the profession have a statutory role in the supervision of pension funds and life insurance companies as well as a statutory role to provide actuarial opinions for managing agents at Lloyd's.

![]()

Damages Discount Rate Consultation 11 May 2017 Ministry of Justice

102 Petty France

London

SW1H 9AJ

Dear Sirs

IFoA response to MoJ Consultation "The Personal Injury Discount Rate"

The Institute and Faculty of Actuaries (IFoA) welcomes the opportunity to respond to this consultation. Members of the IFoA's General Insurance Board have led the drafting of this response.

We have answered the questions to the consultation in the attached Appendix. However, we have set out the main points of our response in this letter.

Discount Rate Methodology

The IFoA believes the discount rate should be set in a way that minimises the risk to the claimant. As such, the rate should be set in line with the yield on index-linked gilts. We have suggested a number of practical solutions to provide some stability in using a market yield.

We have also suggested a formal mechanism for changing the rate that would remove the political sensitivity of making future rate changes.

PPOs

We have also highlighted the benefits of using PPOs for claimants. In particular, we have suggested a number of ways in which providing PPOs could be made easier; thus, providing better outcomes for claimants.

Next Steps

We are aware that you will receive a range of responses that may be challenging to reconcile. The IFoA would welcome the opportunity to discuss our response with MoJ and other respondents in more detail. We recognise the current purdah period would delay any discussions, but we would be delighted to host a roundtable event at Staple Inn Hall , if you believed that would be of value.

If you wish to discuss any of the matters included in our response, you should contact Philip Doggart, Technical Policy Manager, (Philip.Doggart@actuaries.org.uk / 0131 240 1319)

If you wish to discuss any of the matters included in our response, you should contact Philip Doggart, Technical Policy Manager, (Philip.Doggart@actuaries.org.uk / 0131 240 1319)

Yours faithfully

Michael Tripp

Chair, General Insurance Board Institute and Faculty of Actuaries

- The Institute and Faculty of Actuaries welcomes the opportunity to respond to the MOJ's consultation on the Ogden discount rate.

- A number of individual actuaries have contributed to this response, many of whom work in the insurance industry. Whilst our response is informed by the detailed insurance knowledge of our members, its primary focus is the interests and fair treatment of injured parties. Fair compensation, but not over-compensation, is how we interpret the objective of the MoJ in publishing this consultation, and all our comments are directed towards this end.

- Whilst the majority of the numbered questions in the consultation relate to the position of claimants, a few relate to the cost of providing PPOs. The impact assessment also looks at the position of those paying, or paying for by way of insurance premiums and taxes, the compensation. In our response, before proceeding to the numbered questions, we have discussed the challenges facing insurers, since some of these challenges and the long term implications of them may not be widely recognised. We also compare the risk-carrying capacity and investment constraints available to individuals as claimants and to insurers.

- A number of aspects are included in our response, which are not directly addressed by the questions posed in the consultation. They are important to the ability of insurers to fulfil the functions that society expects, but which we believe are not essential for the Government to resolve before coming to decisions about the Ogden rate. However, they are important to understand because they do provide some background to concerns expressed by insurance company managers regarding the difficulty of carrying the risks associated with PPOs.

- Whilst actuaries in practice operate more widely across the economy than used to be the case a few decades ago, the core of the actuarial profession continues to be the meeting and the evaluation of long term financial needs. Indirect consumers of this work are members of the public in relation to insurance of all types and also payments for life such as pension annuities. Actuaries advise on the stewardship of the financial entities that provide these benefits, including questions such as what premiums need to be charged to protect the entities from losses, what are appropriate strategies for their invested assets, what amounts need to be set aside to meet the liabilities, and what additional shareholder capital is needed to protect the entity and all its counterparties from the failure to deliver on the promises it has made.

- In our response to the previous consultation on the discount rate, we set out a number of the principles which we have continued to use in formulating this response.[1] In this present document, we refer to this as "our former response".

- There are two challenges insurers have faced, and still face, in relation to personal injury compensation that we wish to highlight. The first relates to the history of the Ogden rate. Over the years, this has become out of line with market consistent measures. Had the rate been prescribed to a basis that would adjust from time to time to keep it reasonably close to market consistent measures, insurers would have had more certainty, and would have priced their insurance products accordingly

- Now that there has been a sharp change in the Ogden rate, this exposes the fact that there are many past accidents with unresolved liabilities, for which the reserves held have been insufficient. With "long tail" insurance business of this type, there will always be a material lag between the assessment of premiums and the settlement of the losses, so the risk of under-pricing and under-reserving will always be present. However, in the case of the Ogden

rate, the Government could do its part by ensuring that the framework adjusts the rate to reflect investment market conditions much more frequently.

- The second challenge is the accumulation of long term risks within general insurers as the number of PPOs awarded build up. Whilst this is a significant challenge for insurers, we do not believe this important challenge should have any direct impact on decisions relating to the discount rate, however.

Q1 Do you consider that the law on setting the discount rate is defective? If so, please

give reasons.

- We understand that the main principles in the current law, as set out in Wells v Wells, are as follows:

- 100% compensation but not more or less;

- That the claimant should be regarded as very risk averse; and

- The way in which the claimant uses the compensation is not relevant to its determination.

- As a consequence of this, under the current law, the cost to the defendant is not a consideration in setting the discount rate.

- In our former response, under Question 3 of that consultation, we expressed the view that a market-consistent basis is appropriate. Quoting from this, "A market-consistent approach does not take into account the actual assets held, but relies on market information at the date of the transaction to determine the discount rate." This approach would lead to a focus on risk free rates of return, as was favoured by their Lordships in Wells v Wells when they set the discount rate by an inspection of Index-Linked Gilt yields.

- Whilst there is an argument that the degree of risk aversion of claimants is likely to vary for different heads of claim, the largest damage awards will normally relate to cost of care for the rest of the claimant's life, which is an absolute necessity. The "very risk averse" principle recognises this. We also note that the impact of any discounting calculation will be greater for such "rest of life" necessities than any other heads of claim. In some cases, "case management" expenses may have a "rest of life" character.

- For loss of earnings, one could make the argument that, depending on how high the individual's earnings would have been, there could be scope for the individual to take a less risk-averse investment strategy as not all of the earnings may be needed to cover basic needs. So it could be argued that the "very risk averse" position could be relaxed for loss of earnings. Apart from loss of pension, other heads of claim, however, will tend to be for specific costs, with little scope for the claimant to avoid them.

- One of the specific challenges in using the yield on index-linked gilts as a measure of a risk- free rate is that RPI may not necessarily be the ideal match for the rate of increase in liability costs. As the lump sum will reflect different heads of damage, compensation payments as they fall due would increase at different rates. While it is impossible to remove this mis-match in a simple system, we would support the use of an inflation-linked (currently RPI) measure as a proxy for those rates of increase.

- The ONS has indicated that RPI is less accurate and tends to over-state inflation compared to CPI-based measures due to the methodology used for its calculation. Given that ILGS bonds are RPI-linked, government could alter the discount rate to reflect an appropriate inflation-

linked measure. Such a measure could reflect the inflation mis-match, the potential of reinvestment risk or even incorporate an adjustment to reflect how an insurance company would price a PPO. If the Government were to adopt such an approach, we would hope to have a transparent methodology that would be easily understood. We would also expect such a methodology to be open to regular review.

- We will expand on the different situations of insurer and claimant later in this response, but a useful "sense check" for the fairness of a lump sum is to compare it to an alternative such as a PPO. This may indicate whether the insurer has a strong financial incentive to prefer a lump sum over a PPO, or vice-versa. If this is the case, whilst the law may not be "defective", it could still be argued that it is not working as intended.

- In our former response, we expressed our strong support for the use of PPOs wherever possible since they often best meet the needs of the claimant. Only a PPO can deal with the uncertainty over how long the claimant will live, and it also provides a more appropriate means of dealing with long term inflation risk. Claimants in jurisdictions where PPOs are not available do not have this advantage.

- It is important to appreciate that even if the post-tax, post expenses, investment return achieved on the investment of a lump sum award matches the Ogden discount rate, the claimant is still exposed to longevity risk if they live longer than average. This risk is removed by PPOs. We are not convinced that claimants who accept lump sums when a PPO is available always understand this. Insurers have greater scope to manage longevity risk by pooling it in a way that individual annuitants cannot.

Q2 Please provide evidence as to how the application of the discount rate creates under-

or over-compensation and the reasons it does so.

- We are unable to provide individual case studies of claimants' experience of investing their lump sums and their success as investors. Other respondents may be better placed to do so. However if there were no change in the law, any such cases would, in our view, not invalidate the principle that a risk-free strategy was the appropriate benchmark from which to judge fair compensation. On that basis, however, if the Ogden discount rate is materially out of line with forward-looking index-linked investment returns for the expected cash flow profile of the claimant, that in itself will give rise to either over- or under- compensation when a lump sum is taken. Prior to the recently announced change in the discount rate, we would suggest that with reference to the principles underlying the current law, accepting lump sums either gave rise to material under-compensation, or required claimants to invest in a range of more risky assets than was considered when the rate was set at +2.5%.

Q3 Please provide evidence as to how during settlement negotiations claimants are

advised to invest lump sum awards of damages and the reasons for doing so.

- We are not in a position to give evidence on this.

- As a general point, for all of the questions in this section that ask for evidence of what actually happens at the claimant level, we think that independent expert pro-active research would be the best way for the MoJ to discover the facts and to make a balanced assessment. That would mean interviewing the different parties and their advisers in a sample of cases, and also studying case files. This suggestion is also relevant for questions 4, 5, 6, 7 and 9.

Q4: Please provide evidence of how claimants actually invest their compensation and their

reasons for doing so.

- Please see our response to Question 3.

Q5 Are claimants or other investors routinely advised to invest 100% of their capital in

ILGS or any other asset class? Please explain your answer. What risks would this strategy involve and could these be addressed by pursuing a more diverse investment strategy?

- For the first part of this question, we refer to our answer to Question 3.

- Regarding the second part of this question, it is important to be clear what presumptions may be behind the question. In actuarial work, the setting of valuation assumptions in a matched cash flow exercise suggests a market consistent approach. This is a very distinct question from what the investment strategy may be. The related issues were covered within our earlier response.

- This may be a good point to explore the relative situations between an insurer and a claimant if we were to use a forward-looking and subjective evaluation, i.e. to depart from the simple risk-free, market-consistent model.

- The insurer:

- Will have free capital, allowing it to take more investment risk than an individual if it chooses;

- Will be a "gross" taxpayer, in that expenses such as those relating to investments will be offset before it pays tax;

- Will have investment expertise that is efficiently applied to a large portfolio of assets; and

- Will be able to pool longevity risk.

- The claimant:

- Will normally have no free capital;

- Will receive non taxable PPO amounts; but all investment returns on invested sums are taxable above certain personal allowance thresholds. If the lump sums are large and the investment income, or any capital gains, are substantial, this could be significant; and

- Is likely to need advice, or delegation of investment management. The cost of this is not deductible from taxation. The total costs of investment and financial advice and investment management will be substantial (these matters are explored in depth in various studies made by the Financial Conduct Authority).

- Another practical question relates to the challenge of making judgments of forward-looking investment returns at any point in time. Whereas for index-linked gilts, one can assess precisely what real return is built in over the length of each instrument, simply by looking at the market price of the instrument today. No similar model exists for any other assets with regard to real returns.

- In the previous paragraphs we focused on the claimant. It is also important to consider relative position of the insurer and the claimant. We would suggest, having regard to the two sets of bullets above, that the net of tax, net of expenses, net of inflation return available to a risk adverse claimant would be materially lower than that available to an insurer.

- We can also consider the "cost", in terms of assets needed to be set aside to meet the cash flow for a PPO, first if the insurer is going to provide the PPO, or second if the claimant takes a lump sum and self-funds the necessary cost of care cashflow themselves. It is difficult to understand how the lump sum for the claimant could be anything other than materially greater than the amount of assets the insurer would need.

- This analysis suggests that in order for a claimant to expect to achieve the same return as an equivalent PPO in the event that the law had regard to the probable fully net (i.e. of tax and expenses) investment returns achieved by the claimant, any lump sum paid would need to materially exceed the amount the insurer would need to hold in reserve for the PPO. Similar principles will apply to the discounting of all future sums using the Ogden tables.

- Returning to the existing law, prior to the latest change in the Ogden rate, insurers were in recent years able to make very material savings, compared to PPO reserves, when claimants accepted lump sums. It will take many years before we know the extent of such savings against PPO payments actually paid. However, this situation appears anomalous and inequitable to claimants.

Q6 Are there cases where PPOs are not and could not be made available? Are there cases

where a PPO could be available but a PPO is offered and refused or sought and refused? Please provide evidence of the reasons for this and the cases where this occurs.

- In public discussion of PPOs, we think there is a common misconception that claims are settled "either" as a PPO, "or" as a lump sum. It is important to recognise the general point that PPOs are almost always in respect of cost of care only, though case management costs may be included. That always leaves many other heads of claim that are settled by lump sum. So whilst cases without PPOs will be settled by lump sum, there will be no cases that are settled only by a PPO. The PPO element is likely to be the most important part of the total cost, when a PPO is part of an award, However, there are a number of situations where a PPO would not be made available. Most of these revolve around the compensation level being limited. In addition, claimants in Scotland do not have the same benefits in law in relation to PPOs that other claimants have elsewhere. Examples include:

- Where the provider is considered insecure, such as insurance not protected by the FSCS, thus the claimant cannot be guaranteed future payments and hence a lump sum is considered more appropriate.

- An element of contributory negligence would decrease the level of compensation made. The annual payments may be insufficient to cover the care needs. Thus the claimant may wish for a lump sum so that they can maintain flexibility around provision of care.

- Where there are fixed limits of indemnity. If the lump sum is sufficiently close to the limit, then the claimant would get a greater present value of compensation from a lump sum than a PPO as the limit would be exhausted under a PPO at a later date, thus providing a lower present value.

- In our former response, we mentioned the possibility of requiring unlimited cover more widely to protect claimants from under-compensation.

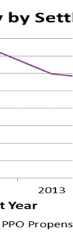

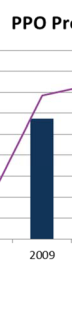

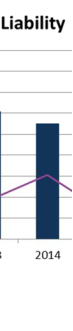

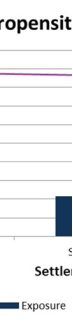

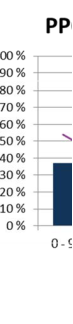

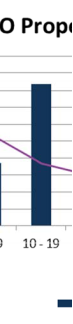

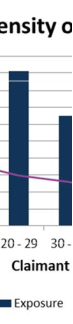

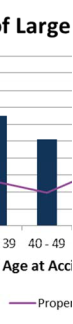

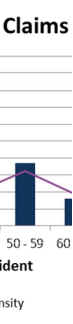

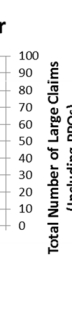

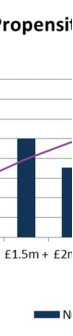

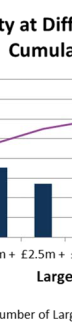

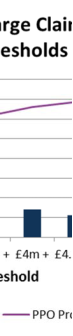

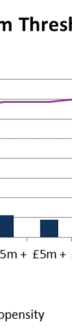

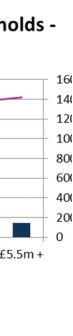

- We understand that there are cases where a PPO would be available but is not taken up. We have no specific information as to the reasons. However the graph below shows how the propensity of PPOs in liability claims tends to decrease with the increasing size of the award, notwithstanding the previous comments about the availability of PPOs. It would therefore seem that one relevant consideration is the size of the total award, as a proxy for the severity of the injuries or financial loss to the claimant.

Q7 Please provide evidence as to the reasons why claimants choose either a lump sum or

a PPO, including where both a lump sum and a PPO are included in a settlement.

- As noted in our response to question 3, we do not have evidence of claimants' choices. We have also noted there may have been incentives for insurers to settle purely by lump sums and avoid PPOs. This may have influenced the negotiations and settlements.

- We would repeat the point made above that, as well as the cost of care, there are many other heads of damage that are met by providing lump sums. Homes may need re-engineering, for example, and special equipment may be needed. In practice, PPOs rarely cover anything other than cost of care, so lump sums are inevitable.

Q8 How has the number of PPOs changed over time? What has driven this? What types of

claims are most likely to settle via a PPO?

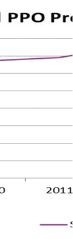

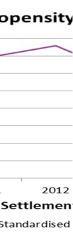

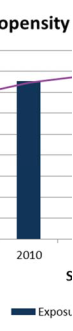

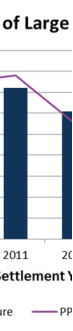

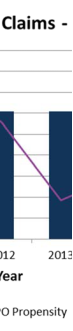

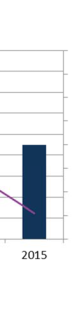

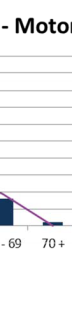

- The number of claims increased dramatically after the Thompstone judgement and financial crash. There was a peak in 2012 but the proportion of claims settling as a PPO has fallen since.

- This graph shows the propensity of PPOs for motor by settlement year:

![]()

![]()

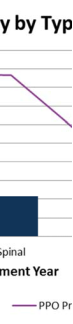

- This graph shows the propensity of PPOs for liability claims

![]()

- It is not certain what has driven the change in propensity, but proposed reeasons for the reduction include:

- ASHE was close to zero for a number of years (including negative vaalues), which may have depressed the appetite for PPOs;

- There may have been a backlog of claimants wanting to settle as a wwage linked PPO, which caused a high volume of PPO settlements following the Thompstone judgement;

- Insurers have increasingly sought innovative options to settle a claimm as a lump sum, e.g. contributory negligence, accommodation etc;

- Uncertainty over the future discount rate as a result of the ongoing coonsultations may have caused a lag in PPO settlements, as those undecided may havve delayed settlement (where possible) in anticipation of a drop in the discount rrate; and

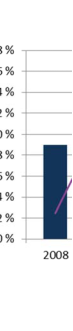

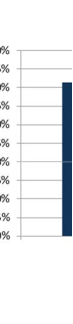

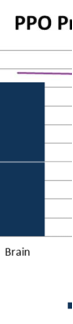

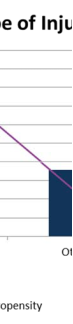

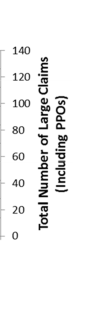

- The claims most likely to become PPOs are those where the claimant is aa minor, or has suffered a severe brain or spinal injury. We would expect intrinsically thatt for brain injury claims, there would be a higher propensity to take PPOs than for spinal innjury claims, due to the requirement for a judge to opine on the compensation for patients. Hoowever, the graph below shows that where data is available, the propensity across both typees of injury is consistent. It is possible that there is a distortion by age or by losses with multiple injuries due to inconsistent coding of the injuries. There would appear to be a correlaation that the large claims tend to be more likely to settle as a PPO, as the younger claimantss, and those with major brain and spinal injuries would tend to have the largest claim amouunts.

![]()

![]()

![]()

![]()

Q9 Do claimants receive investment advice about lump sums, PPOs andd combinations of

the two? If so, is the advice adequate? If not, how do you think the ssituation could be improved? Please provide evidence in support of your views.

- We refer to our response to question 3 as we do not have evidence to proovide an answer to this question. As PPOs remove much of the risk that a claimant faces commpared to a lump sum payment, we believe that those representing claimants should have a very clear duty to explain the PPO option. We would encourage representatives to adequattely explore PPOs before any decision to take an alternative lump sum.

Q10 & Q11 Do you consider that the present law on how the discount raate is set should be

changed? If so, please say how and give reasons. If you think that tthe law should be changed, do you agree with the suggested principles for setting the rate and that they will lead to full compensation (not under or over compensation)? Pllease give reasons.

- We believe thjs should be a matter for Government having considered thee responses.

Q12 Do you consider that for the purposes of setting the discount rate thhe assumed

investment risk profile of the claimant should be assumed to be: (a) Very (Wells v Wells) (b) Low risk (a mixed portfolio balancing low risk investmentss). (c) An ordinary prudent investor (d) Other.

Please give reasons.

- We explicitly confirmed in our former response that the setting of the disccount rate is a matching exercise and this would naturally lead to a market consistent rissk free basis. This would align most closely with option a. However as highlighted in our respponse to question 1, the exact amount and duration of the cashflows is uncertain.As we notedd, the policy intention that, on average, a claimant does not suffer gain, or loss, is a reasonablee compromise, which the Ogden table methodology recognises.

- We would again emphasise that there is no perfect matching asset class as the duration and the cashflows required remain uncertain, but a PPO alleviates some of these issues.

Q13 Should the availability of Periodical Payment Orders affect the discount rate? If so,

please give reasons. In particular: Should refusal to take a PPO be taken as grounds for assuming a higher risk appetite? If so, how big a difference should this make to the discount rate? Should this assumption apply in cases where a secure PPO is not available?

- If a claimant chooses not to take a PPO, that may indicate a willingness to accept some investment and/or longevity risk. Such a decision should not impact the selection of a discount rate because of the uncertainty that remains with the claimants who accept lump sums. In Scotland, claimants are relatively disadvantaged.

Q14 Do you agree that the discount rate should be set on the basis that claimants who opt

for a lump sum over a PPO should be assumed to be willing to take some risk? If so, how much risk do you think the claimant should be deemed to have accepted? Please also indicate if you consider that any such assumption should apply even if a secure PPO is not available. Please give reasons.

- There are risks associated with taking a PPO which the claimant may be balancing with those risks associated with a lump sum. These risks will be very specific to the individual case. As most lump sum settlements are reached by negotiation, a claimant's preference for a lump sum may be a factor in the settlement process. However, we repeat our view that such a preference should not impact the discount rate.

Q15 Do you consider that different rates should be set for different cases? Please give

reasons. If so please indicate the categories that you think should be created.

- We need to be careful about seeking what may become a spurious level of accuracy in practice. There is no computational reason why a very complex set of differing discount rates could not be applied to different compensation drivers. The negotiation aspects of any settlement could simply lead to this generating more grounds for argument and hence further complicated settlements. There are benefits in having a simple framework based on a single discount rate.

Q16 Please also indicate in relation to the categories you have chosen whether there are

any special factors that should be taken into account in setting the rate for that category.

- We refer you to our response to question 1 considering potential options to reflect any mis- matching between the discount rate and actual payments.

Q17 Should the court retain a power to apply a different rate from the specified rate if

persuaded by one of the parties that it would be more appropriate to do so? Please give reasons.

- Although this power is currently available we understand it is not exercised. Retaining such a power could create scope for satellite litigation, although there is little evidence to date that is has.

Q18 If the court should have power to apply a different rate, what principles should apply to

its exercise?

- In order to provide certainty to claimants and compensators, we would expect the courts to use any discretion rarely. This means that different rates would only apply in very exceptional circumstances. If this were not the case, it may prove an impediment to swifter settlements in general.

Q19 Do you consider that there are any specific points of methodology that should be

mandatory? Please give details and reasons for your choice.

- We would reference our response to question 1, where we emphasise the importance of setting the discount rate in a market consistent and risk-free manner.

Q20 Do you agree that the law should be changed so that the discount rate has to be

reviewed on occasions specified in legislation rather than leaving the timing of the review to the rate setter? If not, please give reasons.

- If the discount rate were linked to a defined index (such as long-term ILGs), there would be the option to review the basis of the rate only if it had changed by more than a defined amount. The exact permissible variation would be to strike a balance between fairness of payments, to both parties, and simplicity of approach. In view of the great sensitivity of the Ogden factors to small changes in discount rate, we would suggest that once the currently used rate becomes out of line with market conditions by more than 0.25% the rate should be changed. We would also note, as pointed out in our earlier submission that the fair and correct approach is to use is a current, forward-looking market rate rather than having regard to a historical average.

- Alternatively, fixing the frequency of review may seem attractive in providing clarity as to when the discount rate may change, but is likely to result in a hiatus, or rush to, claims settlements as such a date approaches. Either party may potentially see a benefit from waiting until the date of change to settle a case. We understand that following the recent announcements, there were clear examples of claim settlements stalling from December onwards, as claimants correctly anticipated a more favourable settlement after the announcement. The downside of such an approach is that a defined discount rate may not be consistent with current market rates, which in effect, replicates the current situation, although a market consistent rate mitigates this.

Q21 Should those occasions be fixed or minimum periods of time? If so, should the fixed or

minimum periods be one, three, five, ten or other (please specify) year periods? Please give reasons.

- If our suggestion about only reviewing the discount rate if the index varied by more than a defined amount were adopted, this would remove the need for a formal review. This would ensure that discount rates remained closely aligned to the market rate.

- If the discount rate took account of mis-matching by including a fixed adjustment to the market rate, as discussed in relation to question 1, it would be appropriate to review that variation. A regular review, perhaps once during each Parliament, would ensure the discount rate reflected changes to the relevant factors.

Q22 When in the year do you think the review should take effect? Please give reasons.

- Our proposal in response to question 20 would remove the need for such a review

Q23 Do you agree that the rate should be reviewed at intervals determined by the

movement of relevant investment returns? If so, should this be in addition to timed intervals or instead of them? What do you think the degree of deviation should trigger the review?

- Our proposal in response to question 20 would remove the need for such a review to validate the effect of sudden market movements.

Q24 Do you agree that there should be a power to set new triggers for when the rate should

be reviewed? If not, please give reasons.

- Our proposal in response to question 20 would automatically trigger a review

Q25 Do you consider that there should be transitional provisions when a new rate is

commenced? If so, please specify what they should be and give reasons.

- Transitional provisions are unlikely to be easy to apply and are difficult to justify. If a rate change is triggered it would be better to keep the period of consultation / review as short as possible so as to minimise the impact of settlements and then move forward with the new agreed rate as soon as possible for all settlements after that date.

Q26 Do you consider that the discount rate should be set by: a) A panel of independent

experts? If so, please indicate how the panel should be made up. b) A panel of independent experts subject to agreement of another person? If so, on what terms and whom? Would your answers to the questions above about a panel differ depending on the extent of the discretion given to the panel? If so, please give details c) The Lord Chancellor and her counterparts in Scotland or another nominated person following advice from an independent expert panel? If so, on what terms? d) The Lord Chancellor and her counterparts in Scotland as at present? e) Someone else? If so, please give details.

- Our proposal in response to question 20 would remove the need for such a review. We would also emphasise the need to review any fixed adjustment to the market rate. We would encourage the Lord Chancellor to use an independent expert panel.

Q27 Do you consider that the current law relating to PPOs is satisfactory and does not

require change? Please give reasons.

- There are two areas to consider here:

- How the PPO details are framed; and

- How they are mandated.

- In terms of how they are framed, there is flexibility of the courts to vary PPOs, for example in respect of rate. The current case law suggests the use of ASHE 6115 and its successor, which links the PPO indexation to carers' wages. This has benefits and disadvantages.

- The main disadvantages are to policyholders of insurance contracts. Insurance companies who have PPO liabilities are unable to invest so that they can match ASHE, which, in turn, means that these insurers have to hold a greater amount of capital than they would otherwise.

Their reinsurance contracts are less effective in these cases due to the way that the retention levels themselves index. Over time, the balance sheet of a general insurance company will become more and more like that of a life insurance company. This inefficiency means that the premiums paid by society are higher than they might otherwise have been. The many paying for the few is the nature of insurance and hence might seem appropriate. However the increased cost might be disproportionately spread, and may cause some specific groups of drivers' premiums to rise to the extent that it becomes uneconomical to insure their vehicles. Also it means that insurers are more likely to fail, which could ultimately fall back on the State.

- There is a benefit in the linking to ASHE for the claimants, as it is likely to be the best match available under the current compensation regime. Moving to a form of compensation where an agreed number of hours of care is set, for which the claimant obtains quotes and the insurer pays the provider directly, would provide compensation that indemnifies the claimant, but would likely come with a direct impact on the cost of purchasing insurance.

- While an inflation link is a benefit for the claimant, ASHE is not a perfect match to the liabilities. Basis risk remains with the claimant, as the ASHE being a survey is influenced by changes in the makeup of the constituents. For example, for an individual care worker in the 80th percentile, they are likely to have seen some increase or at worse a level payment, whereas the ASHE 80th percentile has fallen, arguably driven by immigration of cheaper workers from the EU.

- The law relating to mandating of PPOs allows those with the capacity in the eyes of the law to make their own decisions as to the compensation. Most will typically have advice as to what to request from IFAs, etc. Not mandating, however, opens up the possibility of a moral hazard, in that a claimant may take up the lump sum and spend it ahead of time, safe in the knowledge the State will pick up the care if the money runs out. This may also result in the claimant not making the decision about the form of compensation such that is most likely to result in their long term needs being met from the compensation, as the State will step in if the compensation runs out.

- There is a wider problem facing claimants, and arguably also defendants, that arises from the adversarial character of dispute resolution. Faced with an offer which, if rejected and which the court subsequently upholds, a claimant may find themselves in difficulties if there is a significant additional bill relating to legal expenses of the defendant. The reverse applies, of course, but the defendant is better able to "throw the dice" and play the percentages. Alternative dispute resolution processes whereby, for example, an independent expert is appointed to advise the court, could give faster, better, and also cheaper justice.

Q28 Do you consider that the current law relating to PPOs requires clarification as to when

the court should award a PPO? If so, what clarification do you consider necessary and how would you promulgate it?

- The current approach appears fair in that judges have the power to enforce them in all circumstances, and that a judge must consider them in the cases where the claimant does not have legal capacity, whether mental, or due to age. Thus the claimant has flexibility to make their own decisions under expert advice. As discussed in our response to question 9, those representing claimants should have a very clear duty to explain the PPO option and ensure this is adequately explored before any decision to take a lump sum payment instead.

Q29 Do you consider that the current law relating to PPOs should be changed by creating a

presumption that if a secure PPO is available it should be awarded by the court? If so, how should the presumption be applied and on what grounds could it be rebutted?

- The advantages of this option include:

- This takes away some of the problems with achieving the aim of 100% compensation, without over or under compensating, as it addresses the longevity risk.

- The Government and NHS can be more confident charges will not fall back on them as the claimant is covered for life; however, some PPO claimants will, in any case, be entitled to an element of statutory funding.

- Whilst one may argue that there are benefits to insurers from the certainty about whether claims would be settled as PPOs, the greater uncertainty associated with PPOs in payment is likely to override this.

- Less scope for insurers/lawyers to avoid this route when it is the most beneficial for claimants.

- Individuals tend to value amounts in the near term much more than amounts in the future. This may cause them to make an imperfect decision even with the existence of expert advice. This option would potentially reduce this impact to some extent.

- However the downsides include:

- Less flexibility for claimants to choose how to spend their money.

- There is more uncertainty over the ultimate outcome for insurers (see question 27), resulting in either higher premiums, or a greater likelihood of failure for insurers.

- The claimant must maintain a relationship with the insurer, which they may link to the defendant, and thus be undesirable for the claimant.

- Life insurers are not interested in these products - it is entirely possible that the PRA would not authorise a life insurance company to take these risks. Also the expectation that the PRA would not authorise the creation of a new composite insurer, yet the courts are transforming general insurers into composites, seems to be a contradiction.

- To have an increased PPO propensity would increase the overall cost of providing the cover, with a requisite impact to premiums. This may cause a greater incidence of uninsured driving, in turn increasing the MIB levy which is borne by other insured drivers through their premiums.

- To maintain the choice of the claimant, any presumption of a PPO should be rebuttable firstly when the claimant or their deputy requests a lump sum. Clear areas where it might be rebutted could be for contributory negligence, statutory funding, unsecure company/insurer, or if the claimant has capacity or needs greater flexibility.

Q30 Do you consider that the current law relating to PPOs should be changed by requiring

the court to order a PPO if a secure PPO is available? If so, what conditions should apply?

- Much of the response to question 29 above applies equally here. The mandating of PPOs in these cases is simply a stronger approach than the presumption outlined previously. Therefore, the same advantages and disadvantages largely apply.

- Not all claims go to court, so there may be a question of how to enforce the law if compensation is settled out of court. If mandating of court approval is also necessary then this would increase the court workload and potentially slow down claimants' access to compensation.

- If costs to those providing the PPOs could be mitigated there may be a greater rationale for mandating these as some of the disadvantages would reduce. We have explored ideas for this in our response to question 31.

Q31 Do you consider that the cost of providing PPOs could be reduced? If so, how.

- There are ways that the cost of providing PPOs could be reduced. We have set out three ideas:

- Making PPOs easier to match by changing how they index (thus reducing capital requirement) – Alternative indexation of PPOs;

- Pooling PPO arrangements including a government, or industry, scheme; and

- Changing the way in which capital is calculated.

- None of these are perfect, and all can be categorised as either a reduction of the capital held to fund for uncertainty – which may lead to a greater chance of an insurer failing - or arguably a reduction in the appropriateness of the compensation.

Alternative indexation of PPO liabilities

- Capital must be held to allow for the cost of claims and also for any uncertainty in the amounts of the claims.

- The current structure of PPOs together with the solvency legislation around them makes them expensive to provide for general insurers. This is because annual increases are typically linked to ASHE. Solvency II enables greater discounting if the liabilities can be "matched". Currently, there are no investment vehicles that have been shown to match to ASHE. As a result this increases uncertainty around whether the assets will cover the liabilities, and also reduces the ability of the insurer to apply mechanisms within the Solvency II regulation [the matching adjustment] that would allow the insurer to take credit for having a matched portfolio.

- The ASHE index of care costs is a survey rather than a well-established index and its values can be unpredictable and not linked with other inflation measures. There are no assets that will match the increases of the ASHE index. Even if the insurer takes the "risk free" investment strategies as described earlier in this response, this will not be considered as risk free under the legislation as the index linked gilts do not match the ASHE index.

- An alternative could be to link PPO indexation to a matchable index, perhaps with a fixed difference, e.g. the indexation might be RPI +/- x%. Thus matching assets might be available and permit a lower discounted value of the liabilities (best estimate, risk margin and capital) in the insurer's balance sheet.

- However, a change to the indexation would not necessarily result in the matching adjustment being available. The longevity risk may be too long to be matched. Changing the indexation basis may be insufficient. In Ireland, there has been a proposal to introduce bonds that are linked to the same escalation rate as the PPO index. A similar proposal may assist insurers in the UK.

Pooling of PPO arrangements

- Another issue for general insurers is the overhead of managing the claims. Many insurers currently have a very small number of large PPO claims, which require different claims processes, and specialist knowledge to handle these claims. There is often separate reporting for these claims (they are considered a life insurance type liability) and so they may use disproportionate management resource and investment considerations.

- It may be that some kind of pooling arrangement could be helpful to smaller insurers. Pooling has a precedent in the Pool Re and Flood Re schemes. For these types of liabilities, there might also be some investment benefit, due to increases in scale that may open up asset classes unavailable to an individual insurer.

- However, private sector pooling is not likely to work due to perceived inequalities between participants, and whether cut-through requirements in solvency regimes would require the same amount of capital. Arguably, such a pool would have no diversification benefits so its own capital requirements may be significantly higher than that of the individual PPOs within their respective companies currently. Government backing may alleviate this, but given the recent experience with Flood Re, there may be no appetite within certain areas of government for such back stop guarantees. Alternatively, an industry levy may provide what is needed.

- Alternatively, a transfer of PPO liabilities with their provisions to a public body would remove any default risk for the claimant and provide certainty in terms of costs to the policyholder. The capital requirement to protect against uncertainty could be replaced by a possible industry levy if the provisions are underestimated (eliminating the risk premium but introducing a possible intergenerational transfer of costs). Transferring the liabilities to the government may provide a short term cashflow benefit to the government, given it does not have to prefund these, as well as reduce the amount of capital held for the liabilities in the industry. This would reduce the cost of meeting them. If the transfer price is set at a market consistent valuation, then on average there would be no additional funding needed by the government and, hence, no shift of wealth between generations. This would:

- Help ensure 100% compensation without overcompensation in respect of the mortality risk;

- Limit the cost to the policyholders;

- Reduce the risk to the claimant of an insurer going insolvent; and

- Provide a short term cashflow benefit to the government.

- Ultimately, the claimant payments need to be met and the fact the government gets money in advance but has to make the payments for many years into the future would bring a burden to future tax payers. This would be similar to unfunded state pension payments.

Calculation of capital

- There may be some scope to review the solvency requirements around PPOs but this should only be embarked upon with care, as it can be complicated, and is part of the Solvency II framework so may have wider implications (e.g. ensuring the UK regime is still equivalent).

- If capital approaches are reduced then passporting into Europe may be more difficult. We are unlikely to influence the European regulation from outside the EU.

- Reducing the capital requirement could be achieved, either by reducing the requirement to value on a market consistent basis, or consideration of uncertainty to ultimate in asset

classes, removing the associated risk margin and considering the probability of payment, rather than one year volatility of market value.

- There is some evidence that the same level of infrastructure bonds gives a much lower probability of the assets being insufficient, compared to government bonds. Thus, the risk of not meeting the liabilities as they fall due is lower, but the amount of capital held is higher. As PPOs cannot be subject to significant swings in cashflow without hyperinflation, uncertainty to ultimate is much more important a consideration than the one year market volatility of assets, which is the basis of Solvency II. A less severe treatment of infrastructure bonds in the Solvency II capital calculation may therefore help companies to invest in these to meet their PPO liabilities.

- Solvency II considers the change in the one year value of the assets to be very important in setting the amount of capital to be held. Where short term fluctuations in market value of assets do not affect the financial situation of the investor, perhaps due to no short term need to liquidate large proportions of the fund, then a prudent investor would likely invest in a diversified portfolio to maximise the return on the portfolio.

Q32 Please provide details of any costs and benefits that you anticipate would arise as a

result of any of the approaches described above.

Alternative indexation of PPO liabilities

- The greatest cost is to the claimant as basis risk would be maintained. Claimants have a basis risk already between their annual payments and changes in the ASHE index. To highlight the issue, we note that recently ASHE has been negative or close to zero, whereas there is not an understanding that the claimants' costs have been static.

- It is also worth noting that the ASHE index was almost stopped and the constituent parts were changed, making comparison across years more challenging.

- There could be costs of setting up and administering any bonds that are set up to be linked to the new inflation such as the introduction of a CPI linked bond.

- The benefits to this approach may be that costs to policyholders are lower through lower 2premiums than would otherwise be the case as benefits to insurers are passed on.

- It may result in greater numbers of claims being settled as a PPO, which reduces volatility in PPO propensity but as noted earlier may be outweighed by the uncertainty that a PPO brings to insurers in comparison to a lump sum.

- A more robust index would be less prone to anomalies, and there would be a better match between assets and liabilities.

Pooling of PPO arrangements

100. There would be a cost of setting up the scheme. There could also be considerable capital

cost within any private sector scheme due to concentration of PPO risks, including ASHE.

101. There may be a cost to the government or industry in the future of a transfer to a government

body, and there would also be a short term cost to the industry of paying a value to a pool to transfer the liabilities.

102. Benefits would be that:

- Investment options might be widened, due to greater scale of the pool versus insurers;

- It may create claims handling efficiencies;

- Reduced cost to policyholders in the event of a government scheme – dependent on the transfer price; and

- Reduced risk to the claimant of the insurer going insolvent if using a government scheme.

- Potentially greater purchasing power in reinsurance negotiations

Calculation of capital

103. There would be a cost of agreeing and writing the new regulation. This may impact on

passporting to the EU.

104. If less capital is held, then the likelihood of insurer default is greater – with knock on impact on

FSCS and potentially government as the backstop.

105. The benefits however include:

- A reduced cost to policyholders from the reduced capital requirements;

- May enable insurers to invest in more risky assets – increasing the investment return and hence potentially the cost to policyholders; and

- Greater investment in equities could result in a boost to company share prices, causing a greater degree of optimism in the economy, hence a greater level of company investment and a boost to the economy.

Q33 Please provide any evidence you may have as to the use or expected use of PPOs in

the light of the change in the rate and more generally.

106. We would expect the use of PPOs in relation to insurance claims to further reduce, potentially

markedly, following the recent reduction in the discount rate. The lump sum awards have increased and so they now look more attractive to claimants. Defendants may see PPOs as more attractive than before but all of the unwelcome characteristics remain. Even if they were now viewed as less costly in an accounting sense than a lump sum, they may still be more costly in the long run due to requirements on the private sector to fund in advance and to hold capital against the risk of outcomes not being as expected.

Damages (Investment Returns and periodical Payments) (Scotland) Bill

Damages (Investment Returns and periodical Payments) (Scotland) Bill

IFoA response to Scott ish Parliament Economy, Jobs and Fair Work Committee

(Business Support Inquiry)

About the Institute and Faculty of Actuaries

The Institute and Faculty of Actuaries (IFoA) is a royal chartered, not-for-profit, professional body. We represent and regulate over 32,000 actuaries worldwide, and oversee their education at all stages of qualification and development throughout their careers.

We strive to act in the public interest by speaking out on issues where actuaries have the expertise to provide analysis and insight on public policy issues. To fulfil the requirements of our Charter, the IFoA maintains a Public Affairs function, which represents the views of the profession to Government, policymakers, regulators and other stakeholders, in order to shape public policy.

Actuarial science is founded on mathematical and statistical techniques used in insurance, pension fund management and investment. Actuaries provide commercial, financial and prudential advice on the management of assets and liabilities, particularly over the long term, and this long term view is reflected in our approach to analysing policy developments. A rigorous examination system, programme of continuous professional development and a professional code of conduct supports high standards and reflects the significant role of the profession in society.

SUBMITTING EVIDENCE TO A SCOTTISH PARLIAMENT COMMITTEE DATA PROTECTION FORM

Name: | Institute and Faculty of Actuaries (IFoA) |

Date: | 7 September 2018 |

Organisation: (if required) | IFoA |

Topic of submission: | Damages (Investment Returns and Periodical Payments) (Scotland) Bill, IFoA Response |

• I have read and understood the privacy notice about submitting evidence to a Committee. • I am happy for my name, or that of my organisation, to be on the submission, for it to be published on the Scott ish Parliament website, mentioned in any Committee report and form part of the public record. • I understand I will be added to the contact list to receive updates from the Committee on this and other pieces of work. I understand I can unsubscribe at any time by contacting the Committee. Non-standard submissions Occasionally, the Committee may agree to accept submissions in a non-standard format. Tick the box below if you would like someone from the clerking team to get in touch with you about submitting anonymously or for your submission to be considered but not published. It is for the Committee to take the final decision on whether you can submit in this way. ☐ I would like to request that my submission be processed in a non-standard way. | |

ECONOMY, JOBS AND FAIR WORK COMMITTEE BUSINESS SUPPORT INQUIRY

SUBMISSION FROM Institute and Faculty of Actuaries

Damages (Investment Returns and Periodical Payments) (Scotland) Bill

General

1. What are your views on the Bill overall? Is legislation in this area required? How far do you think the Bill will achieve what it sets out to do?

- The Institute and Faculty of Actuaries (IFoA) welcomes this opportunity to provide a written submission to the Scott ish Parliament Economy, Jobs and Fair Work Committee's Business Support Inquiry into the Damages (Investment Returns and Periodical Payments)(Scotland) Bill. Members of our Periodical Payment Orders Working Party, General Insurance Standards and Consultations sub- Committee and General Insurance Board have all provided input to our submission. Members of the Working Party, Committee and Board have worked closely on Periodical Payment Orders (PPOs) over the last decade. We have also had actuarial input from those involved in providing advice to claimants and defendants.

- The IFoA agrees that legislation is required in the area. We have previously stated that we believe PPOs to be the better solution for claimants. Claimants should be properly compensated, and the proposed Bill does address some of the issues of the current Bill: allowing PPOs, prescribing the discount rate and prescribing a formal review. Courts in England and Wales have long had the power to order PPOs, whereas in Scotland this has been confined to a small number of agreed settlements. The Bill if enacted would remove this inconsistency in the possible forms of compensation.

- We do not however believe that the approach best meets the needs of the pursuer. In the event of a lump sum, full compensation would not be achieved as the discount rate will be higher than risk-free, and hence the rate will not be consistent with a matching exercise, which is our preferred approach.

Part 1

2. Part 1 of the Bill aims "to reform the law on the setting of the personal injury discount rate in order to make provision for a method and process which is clear, certain, fair, regular, transparent and credible". Is it an aim with which you agree? And to what extent do you believe the reform will achieve all these things – a clear, certain, fair, regular, transparent and credible method and process?

- We support the objective of having 'a method and process that is clear, certain, fair, regular, transparent and credible'. However, the results will not necessarily be certain even though the calculation is specified: the calculation is laid out and very dependent onmarket movements - so situations may arise in volatile markets where the calculation changes sharply, and limited scope is permitted to react within cycles. This means that neither insurers nor claimants will have certainty' because of the market volatility. For example, insurers write their business many years before all claims are finally settled, and the changes apply retrospectively.

- The IFoA has previously commented that the needs of the pursuer should be put at the front of the argument. Therefore the approach, by not considering a risk-free rate as a matching exercise would suggest, is not fair to them. Of particular concern is that an insurer would value the claim for solvency purposes by reference to a risk-free rate; it would seem to be unfair to ask an individual in these circumstances to takemore risk than an insurer, despite this being the sole financial risk to the pursuer, and with no diversification, no shareholders to support, nor access to additional funds.

3. In terms of who sets the rate, the Scott ish Government proposes to have the rate reviewed by the Government Actuary rather than Scott ish ministers (as is the current situation). It believes that this will remove the setting of the rate from the political sphere "where there is the potential for pressure from external interests to attempt to influence the outcome" and "should provide fairness to all parties involved". What are your views?

6. We support the principle that the setting of the rate should be free of political pressure. The market valuation-based approach we propose would be free from such political pressures.

4. The Scott ish Government has chosen to lay down in detail how the rate should be calculated in legislation. Do you support this proposal over the approach taken in England and Wales of leaving much more to the discretion of the Lord Chancellor and an expert panel?

- We also support having a structured approach to calculating the discount rate. Themarket valuation based approach we propose would be free from political pressures and would also be clear and transparent for all to use. We have commented that if the Lord Chancellor retains the power to set the rate in England and Wales, then an independent panel should be used to advise him/her.

- Our understanding of the proposals is that although the assessment of the rate lies with the Government Actuary rather than with Scott ish ministers, the ministers would however retain powers to amend by regulation the Notional Investment Portfolio and/or the impact of inflation to be allowed for. This suggests there remains potential for significant political influence on the discount rate in Scotland.